The One Big Beautiful Bill Act of 2025 (OBBBA) marks the most substantial transformation of U.S. international tax regulations since the 2017 Tax Cuts and Jobs Act (TCJA).

The following summary details six critical modifications to international tax law under the OBBBA, emphasizing implications for foreign entities, anti-deferral frameworks, and the structuring of cross-border enterprises.

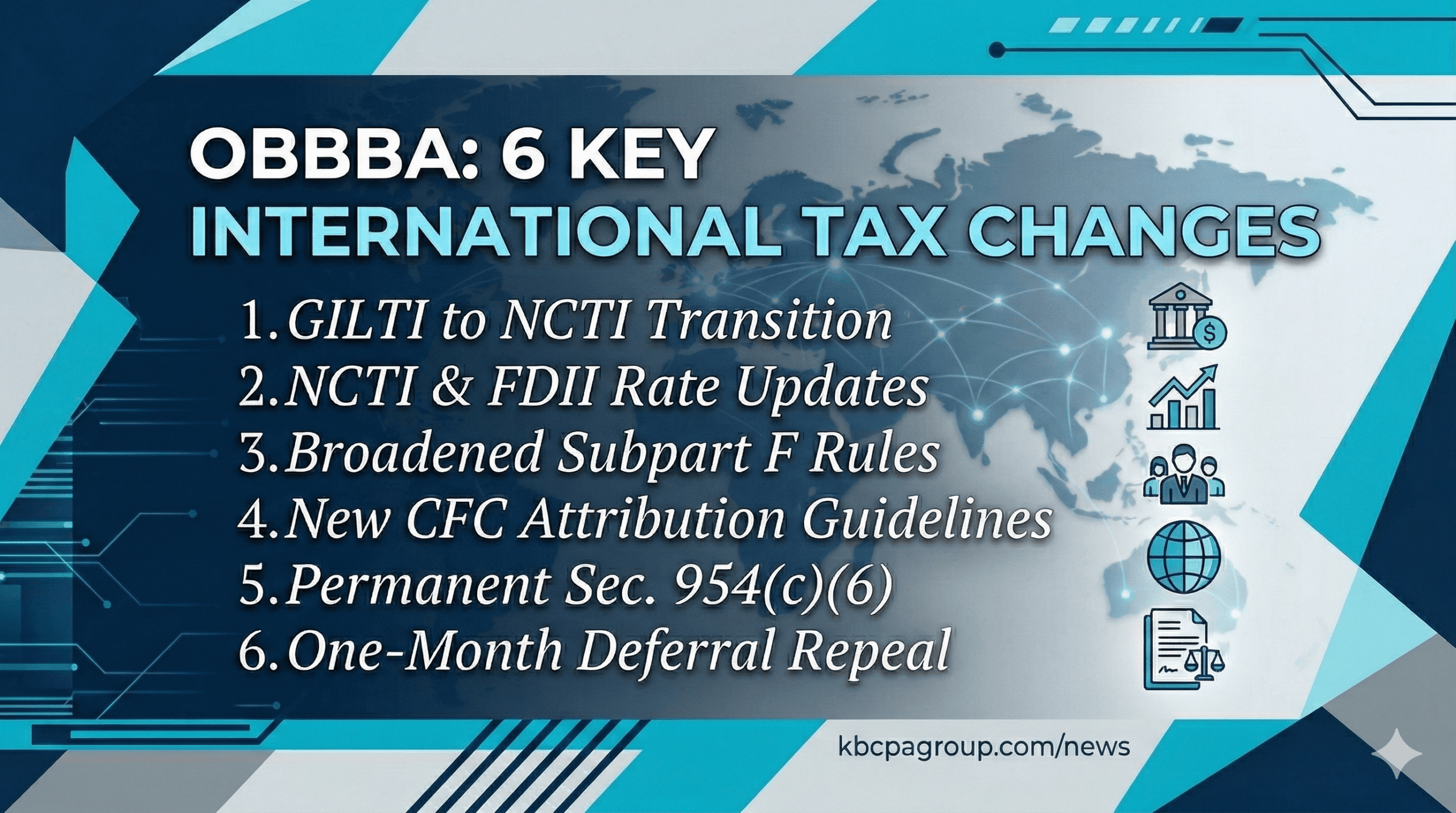

- Transition from GILTI to Net CFC Tested Income (NCTI)

A primary adjustment impacts U.S. taxpayers maintaining ownership or equity interests in controlled foreign corporations (CFCs).

Effective for tax years starting after December 31, 2025, the OBBBA supersedes the Global Intangible Low-Taxed Income (GILTI) framework with a new “Net CFC Tested Income” (NCTI) system.

The NCTI model streamlines reporting by removing the “qualified business asset investment” (QBAI) deduction, which formerly permitted a deemed return on physical assets to be carved out from GILTI. Consequently, all net CFC tested income may now be subject to deemed inclusions regardless of asset composition—creating a simpler, yet potentially more expansive, tax base.

- Revised Rates for NCTI (formerly GILTI) and FDII

Starting in 2026, the effective tax rate for NCTI will rise to 12.6% (up from the 10.5% GILTI rate), driven by a reduction in the Section 250 deduction from 50% to 40%. Conversely, the portion of foreign taxes eligible for credit against NCTI inclusions will improve from 80% to 90%.

Regarding the counterpart to NCTI, foreign-derived intangible income (FDII) for domestic firms currently faces an effective rate of approximately 13.1% (previously slated to hit 16.4% in 2026). The new legislation instead establishes a permanent FDII effective rate of 14%, also taking effect in 2026.

- Expansion of Subpart F Shareholder Inclusion Criteria

Subpart F inclusion mandates have been updated to require U.S. shareholders to report Subpart F income if they hold CFC shares on any day of the taxable year, rather than strictly at the year’s conclusion.

This modification widens the net for Subpart F reporting and eliminates several previous tax planning strategies used to avoid year-end status.

- Adjustments to Subpart F and CFC Attribution Guidelines

The OBBBA restores Section 958(b)(4), effectively prohibiting the “downward attribution” of stock from foreign entities to U.S. entities when determining CFC status.

This measure nullifies a TCJA-era change that frequently resulted in unintended CFC classifications within specific corporate hierarchies.

- Permanent Status for Section 954(c)(6)

Section 954(c)(6), which permits the exclusion of specific inter-CFC dividends, interest, rents, and royalties from Subpart F income, has been rendered permanent by the OBBBA.

Formerly a temporary provision subject to periodic extensions, this permanence offers taxpayers significantly more stability for long-term cross-border structural planning.

- Elimination of the CFC One-Month Deferral Election

Section 898(c)(2), which allowed certain CFCs to adopt a fiscal year starting one month prior to their majority U.S. shareholder’s year, is repealed for tax years beginning after November 30, 2025.

Impacted CFCs are now required to synchronize their taxable years with their majority U.S. shareholders, with specific transitional guidelines managing the distribution of foreign taxes between short and full tax periods.

Conclusion

The OBBBA’s revisions to international tax law are comprehensive and intricate, influencing the taxation of foreign profits, the oversight of CFCs, and the utilization of foreign tax credits.

Organizations with international footprints should meticulously evaluate these new provisions and stay informed on regulatory updates as the OBBBA implementation progresses.